With the EU Chips Act, Europe Enters the Global Semiconductor Race

As countries across the globe ramp up investment in semiconductor production, the EU is looking to bolster its own position.

In February the European Commission presented its proposal for a European chips act which aims to mobilise €43 billion in 'policy-driven investment' for the EU's semiconductor sector by 2030. The plan serves to enable immediate EU coordination against supply disruptions, strengthen and scale up production and innovation throughout the EU semiconductor value chain, and further enhance the Union's technological leadership, practical applications and digital sovereignty in the field of chips. A recent briefing by the European Parliamentary Research Service takes a closer look at the chips act and the European semiconductor sector that it intends to reinforce in the coming decade.

The European chips act proposes to invest €11 billion in research to advance the development of innovative semiconductor technologies. The rest of the funds would target security of supply by attracting investment to develop production capabilities and scale up European semiconductor small and medium-sized enterprises and start-ups. It also proposes regulatory benefits such as fast-track permits for so-called 'first-of-a-kind' facilities. Finally, the chips act provides a coordination mechanism for member states to jointly monitor semiconductor supply chains and collectively respond to disruptions. The Commission here intends to include data-sharing requirements for corporations and semiconductor export controls in times of severe shortages.

The chips act was developed in response to the global shortages and resulting factory closures during the coronavirus pandemic from early 2020 onwards. These events dramatically exposed the vulnerabilities in the semiconductor supply chain and the vital role of chips in modern economies. Delays in chip supplies of up to a year or more caused European car manufacturing to drop 34% from 2019 figures – back to 1975 levels. Industrial equipment producers, healthcare, security, defence and aerospace all suffered from the semiconductor shortages. European car manufacturers hit by the shortages called for increased EU chip production and reduced reliance on imports.

But Europe is not the only player to double down on semiconductor manufacturing. The EU chips act will have to compete or find synergies with existing investment strategies in the US and East Asia. The US and Japan have announced investment plans worth $52 billion and $6.8 billion respectively to attract advanced chip manufacturers, including Taiwan's TSMC, to build production facilities within their borders. China is reportedly providing $97 billion in national and regional funds for the 2014–2024 period, and South Korea has introduced 6–10% tax breaks and other measures, in efforts to attract another $225 billion and $450 billion in Chinese and Korean investments respectively over a 10-year period.

Severe disruption in the supply chain could deplete Europe's limited chip reserves within a few weeks, which would cause production in many European industries to grind to a halt

The proposed European chips act is still awaiting approval as the European Parliament and Council are preparing for negotiations to amend it, but Europe, meanwhile, has already managed to attract huge foreign investments in its semiconductor ecosystem. Recently the US chip manufacturer Intel announced a €33 billion investment to build two foundries in Germany, expand a foundry in Ireland, acquire a foundry in Italy and expand research facilities in France, Poland and Spain, as part of its plan to invest up to €80 billion in the European semiconductor sector in the coming decade. Intel identified the European chips act's expedited permits for the quick construction of advanced facilities as one of its most tangible advantages over the US CHIPS for America Act.

Taiwan's TSMC, the chips giant that accounts for 54% of the global semiconductor market and produces 86% of chips under 10 nanometres, could be the next to invest in building up the EU's chip manufacturing capacity. Taiwan's chip giants are expanding their foreign assets and have so far been building production facilities in the US and Japan. Preliminary talks with German officials took place following the intention expressed by TSMC and Taiwan's foreign minister to establish a foundry there and engage in semiconductor cooperation in Europe. Taiwan welcomed the EU chips act as an opportunity to facilitate such efforts. Europe remains keen to draw in Taiwanese chip investments and cooperate on semiconductor supply chain security. In this context, an online trade and investment dialogue took place in June 2022 between the European Commission's director-general for trade, Sabine Weyand, and the Taiwanese minister for economic affairs, Wang Mei-hua.

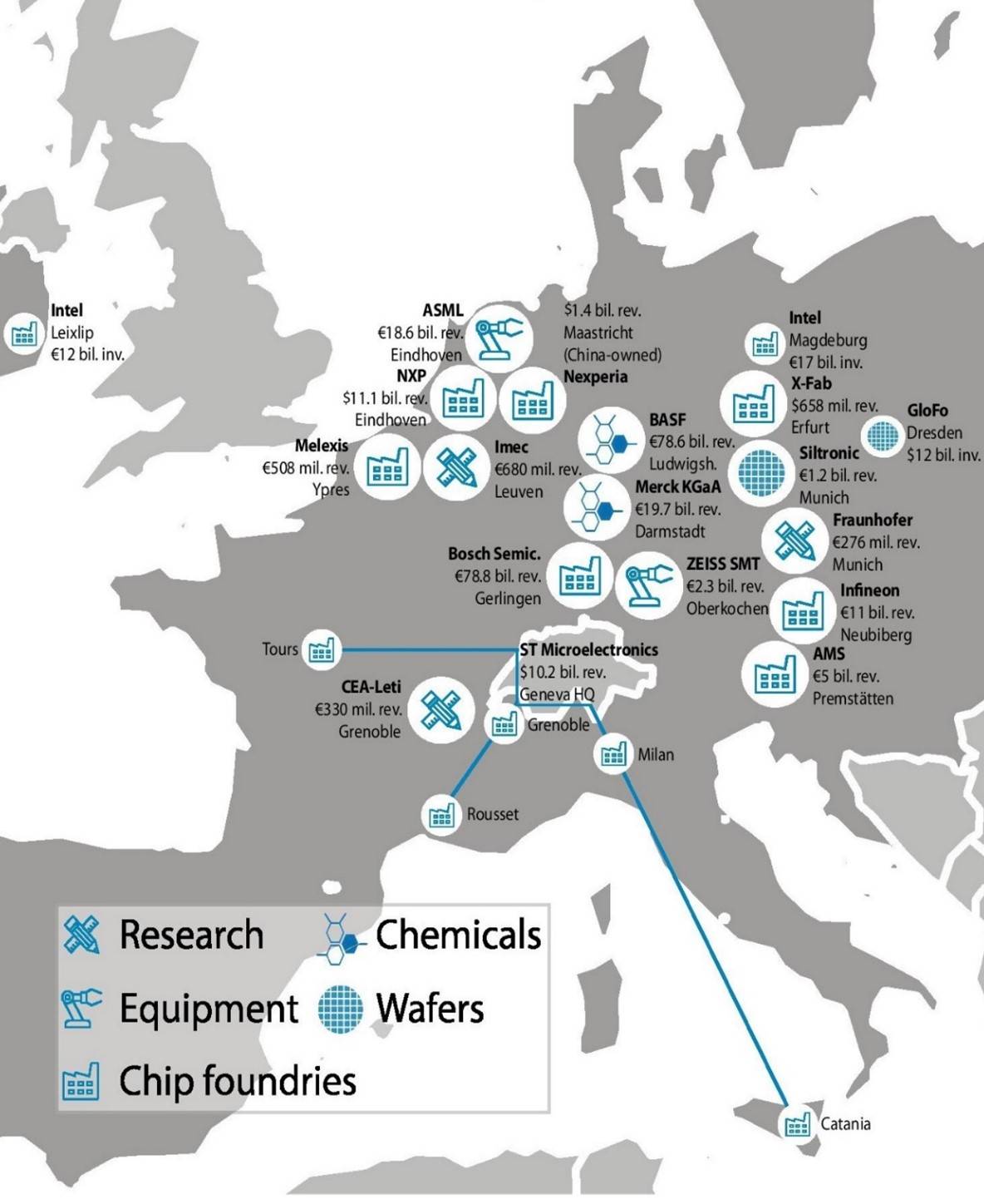

Figure 1: Major European semiconductor assets, annual revenues and foreign direct investment

What makes Europe a viable destination for new semiconductor fab investments is above all its capabilities on the front end of the chip value chain. Europe is home to world-leading semiconductor organisations, including ASML in the Netherlands, the only company that builds the equipment used by TSMC and Samsung to produce the smallest chips. This company is so vital in the global value chain that the US has been pressuring it to stop doing business with China in attempts to put a brake on Chinese technological advances. Europe also has world-class innovative research facilities including Imec in Belgium, Leti in France and Fraunhofer in Germany. German companies also have significant market shares in supplying advanced chemical inputs and wafers for semiconductor production. European chipmakers already own a 37% market share for semiconductors used in the automotive sector, followed by the industrial sector with a 17% global market share. The high semiconductor demand of Europe's car industry, and its future need for more advanced and energy-efficient chips to build into electric and self-driving cars, provides a key destination for manufacturers looking to invest in Europe and sell large quantities of chips produced there by newly constructed fabs.

Figure 2: Global semiconductor market shares

While the EU accommodates semiconductor giants in equipment and research, the EU remains highly dependent on foreign suppliers. Severe disruption in the supply chain could deplete Europe's limited chip reserves within a few weeks, which would cause production in many European industries to grind to a halt. Under 10% of global semiconductor production occurs in Europe, which is limited to the larger chips (22 nanometres and above), and this is down from 20% in the 1990s. Without rapid and significant investment, the EU's global market share could drop below 5%, putting its industrial competitiveness and technological autonomy further at risk and making European chip manufacturing virtually irrelevant on a global scale.

Europe needs to mitigate its growing dependence on China for semiconductor assembly, and related risks of espionage and tampering, by reshoring capabilities at the back end of the value chain

Only two companies in East Asia, TSMC in Taiwan and Samsung in South Korea, are capable of manufacturing leading-edge chips (at 2 to 7 nanometres), while they depend on Europe's ASML for manufacturing equipment. Most European chipmakers outsource their semiconductor fabrication to external foundries, with chip testing, assembly and packaging traditionally occurring in East Asia. Better known European chipmakers, such as NXP in the Netherlands, Infineon and Bosch Semiconductors in Germany, and STMicroelectronics in France and Italy, manufacture the larger chips for the automotive and industrial sectors, but also outsource part of their production to foreign manufacturers like TSMC. While Europe depends on East Asia for advanced chip manufacturing and assembly, European producers also rely heavily on US intellectual property in the form of US-owned chip design tools.

Challenges remain for the EU's chips act to reinforce the Union’s supply security and raise its competitiveness vis-à-vis the US and East Asia. Internally, Europe first of all needs to ensure that its chemical input producers will not be crowded out by China’s subsidisation of its own companies in this sector, as happened with its solar panel industry in the past. Europe would secondly need to mitigate its growing dependence on China for semiconductor assembly, and related risks of espionage and tampering, by reshoring capabilities at these later steps at the back end of the value chain to Europe. Bilaterally, Europe not only needs to attract investments from foreign chip giants such as TSMC, but also to engage in acquiring foreign semiconductor assets. One precedent here is Siemens' 2017 acquisition of Mentor, one of the three main US semiconductor design automation firms holding valuable US intellectual property. Semiconductor partnerships with likeminded countries could facilitate international investment cooperation to expand Europe's chip assets at home and abroad. Globally, Europe needs to foster 'reversed dependency', or in other words enhance foreign dependence on its world-class semiconductor assets in equipment and research. Doing so will prove to be vital in improving Europe's position, leverage and supply security in the global semiconductor value chain.

The views expressed in this Commentary are the author’s, and do not represent those of RUSI or any other institution.

Have an idea for a Commentary you’d like to write for us? Send a short pitch to commentaries@rusi.org and we’ll get back to you if it fits into our research interests. Full guidelines for contributors can be found here.

WRITTEN BY

Kjeld van Wieringen

- Jim McLeanMedia Relations Manager+44 (0)7917 373 069JimMc@rusi.org